Time to Ditch the Card? Open Banking in the United States

Today, Open Banking infrastructure, solutions around the globe are enhancing the customer checkout while promoting cost-savings for merchants.

What is Open Banking?

It is the data transference between and among financial institutions and third parties.

Open Banking allows customers to share their personal account data, such as account balances, spending habits, and cashflow between and among financial institutions and third parties.¹ This is typically done through integration with a payment aggregator², which is authorized by both the account holder to retrieve customer data across various banking services.

It’s also a potentially low-cost payment method.

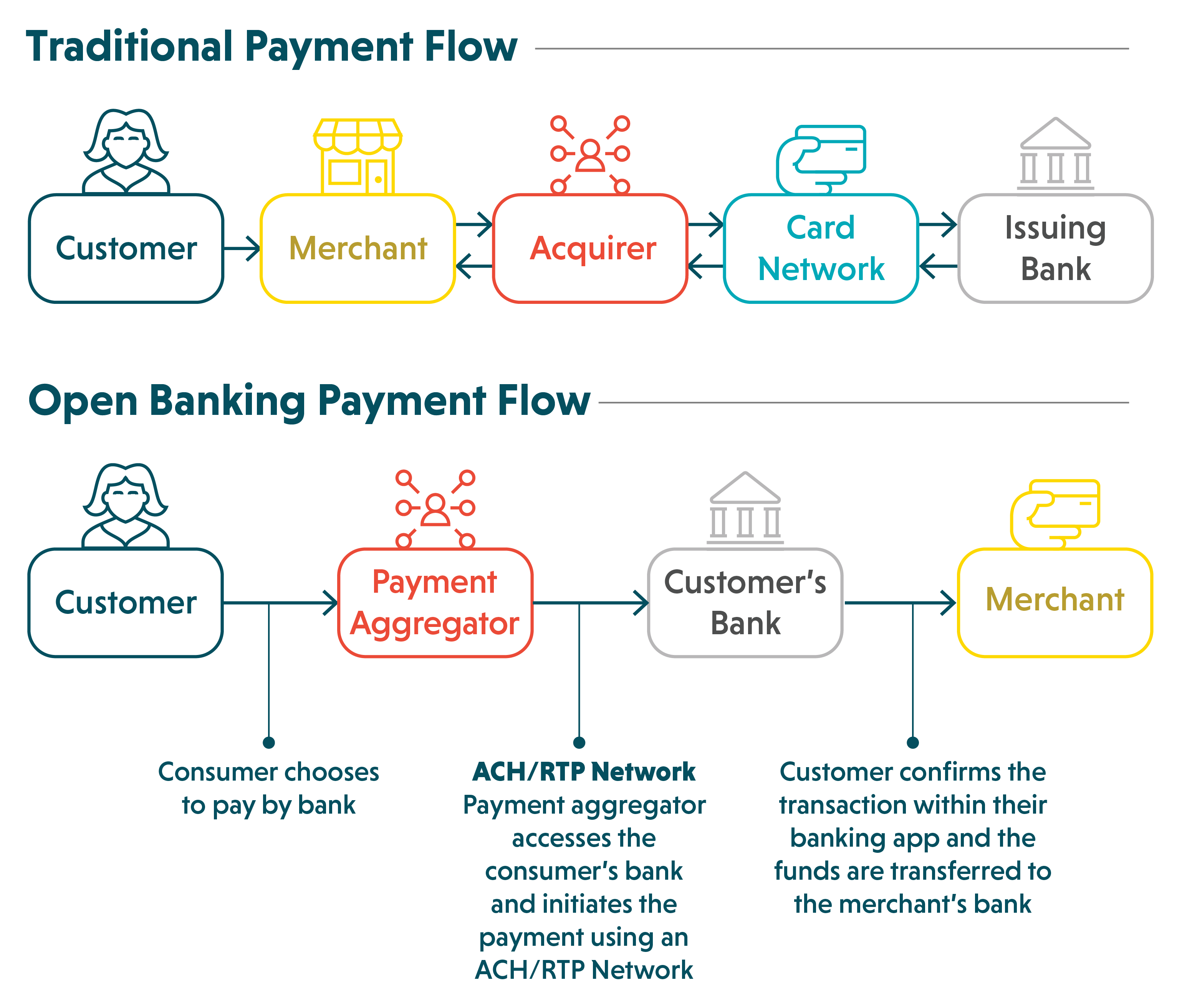

Open Banking also allows customers to initiate payments to third party accounts, facilitating money transfer between consumers and participating financial institutions, third parties, and merchants. This type of transaction can also be facilitated by a payment aggregator³, which is authorized to not only view consumer-permissioned financial data on a bank account, but also make authorized payments on behalf of the customer (Figure 1).⁴For a merchant to receive Open Banking-backed transactions, the merchant must typically either contract directly with a payment aggregator or establish an in-house payment aggregator function.

Why are merchants excited about it?

Cost Savings

Open Banking transactions facilitated by a payment aggregator may represent a bank-to-bank transfer, avoiding the need for an intermediating card network. In the U.S., bank-to-bank transactions such as ACH typically cost merchants between 26 and 50 cents to process5, but can be as low as $0.01 per transaction6, when compared to debit interchange which sit at $0.34.7 It’s anticipated that the Open Banking retail transactions could use an ACH-like bank-to-bank transfer, and as a result, Open Banking could represent a significant savings opportunity for merchants.

Reduced Declined Transactions and Network Fees

Cost savings, however, are only one element of Open Banking’s role in disrupting card payments. Digital account linkages with permissioned read-write access can allow merchants using a payment aggregator to verify customer account balances before a transaction occurs. With this added visibility, merchants may be able to regulate declines associated with insufficient funds – or at the least, avoid assessment fees associated with zero-dollar verification messages.8

Improved Cash Flows for Merchants and Consumers

Merchants and consumers may also see benefits in the form of improved cash flows, as Open Banking solutions around the world use faster payments infrastructures which, in some cases, offer near-instant account settlement.⁹ Lower reported rates of fraud¹⁰ and balanced dispute resolution frameworks¹¹also represent some of the strings in Open Banking’s bow.

Consumer Benefits of Competition

Consumers adopting Open Banking are reported to benefit from increased cross-account transparency, allowing them to gain more insight into their spending habits. Heightened account transparency and portability may also incentivize financial institutions to innovate and compete more to retain customer business.

Unlike pass-through digital wallets, many of which rely on card network infrastructure, Open Banking’s infrastructure and regulatory backing represents a credible challenge to the dominant U.S. card industry.

Open Banking is Coming to the U.S.

Section 1033 within 2010’s Dodd-Frank Act outlined requirements, subject to rules prescribed by the Consumer Financial Protection Bureau (CFPB)12, for financial institutions to provide customers with their own personal financial information, including account balances, transaction history, and other information related to their financial products and services. The sharing of data access “could facilitate competition and innovation in consumer financial services”13and promote portability of account holders, enabling customers to utilize new financial products and services, as well as integrating their data with new fintech companies.

In 2022, there was good news for advocates of a more developed Open Banking regime in the United States. In response to the Biden administration’s July 2021 Executive Order ‘Promoting Competition in the American Economy’, the Consumer Financial Protection Bureau (CFPB)14 released a Personal Financial Data Rights rulemaking in October 2022, outlining proposals intended to fuel market competition for financial services and strengthen consumer data rights.

In remarks pertaining to the rulemaking, CFPB Director Chopra signaled that the Bureau is “shifting away” from compliance burdens associated with complicated rules and policy structures that “fit existing business models”, and instead are “looking to create catalysts for more competition.”15 This involves ensuring customers have greater portability of their financial data as well as more switching and incentives for better financial services and products from financial institutions.

The rulemaking outlines roadmaps for requirements to incumbent institutions to limit restriction for third parties to access consumer-permissioned data, with additional requirements for data recipients to limit misuse and abuse of personal financial data, as well as fraud and scams.

In Q1 2023, the CFPB is scheduled to publish a report about the input received throughout the consultation process which will inform a proposed rule that they are planning to issue later in 2023. The goal is to finalize the rule in 2024 and move to implementation.16

Will 2023 be the year for Open Banking?

While payment aggregator solutions are typically used today for integrations between financial institutions and fintech companies like Robinhood or Venmo, retail payments haven’t seen the same growth opportunities.17 In part, this may be the result of the U.S. representing one of the most developed retail card markets18 and therefore one of the most difficult markets for competitor payments to penetrate. As a result, the cost-saving and competitive benefits of Open Banking have been slow to reach a meaningful share of U.S. retailers. But 2023 may represent change.

Regulators like the CFPB are making competition easier by establishing rules on Section 1033. In addition, the Fed’s launch of FedNow in 2023, a faster payment rail designed to provide an alternative for ACH and card transactions, will offer another comprehensive pay-by-bank infrastructure, in addition to pre-existing infrastructures such as the Clearinghouse, for Open Banking providers to build on. Regulatory developments coupled with competition for user adoption among Open Banking providers could be the fast-track to Open Banking proliferation in the U.S. market as merchants and consumers may look to adopt more accessible, affordable and transparent payment methods.

Sources:

+- https://www.link.money/blog/open-banking-business

- In other jurisdictions such as the UK and EU, this provider is typically referred to as an Account InformationService Provider (AISP), while in Australia, these are broadly referred to as ‘action initiators’

- In jurisdictions such as the UK and EU, this provider is typically referred to as a Payment Initiation Service Provider (PISP), while in Australia, these are also broadly referred to as ‘action initiators’

- https://www.yodlee.com/open-banking/pisp-aisp-open-banking#:~:text=Payment%20Initiation%20Service%20Providers%20in,on%20behalf%20of%20the%20customer

- https://tipalti.com/check-vs-ach-costs/

- CMSPI Estimates and Analysis

- Debit figures pulled from Federal Reserve Reg II data. Credit figures based on Nilson estimates, using a $40 transaction value

- https://www.cardfellow.com/blog/visa-zero-dollar-verification-fee/

- https://www.yapily.com/blog/faster-payments-open-banking

- https://www.finextra.com/the-long-read/420/the-role-of-open-banking-in-the-fight-against-rising-payment-fraud

- https://financialit.net/blog/open-banking/what-businesses-need-know-about-open-banking

- https://www.consumerfinance.gov/rules-policy/notice-opportunities-comment/archive-closed/dodd-frank-act-section-1033-consumer-access-to-financial-records/#:~:text=Section%201033%20of%20the%20Dodd,control%20or%20possession%20of%20the

- https://crsreports.congress.gov/product/pdf/IN/IN11745

- https://www.consumerfinance.gov/about-us/newsroom/director-chopra-prepared-remarks-at-money-20-20/

- https://www.consumerfinance.gov/about-us/newsroom/director-chopra-prepared-remarks-at-money-20-20/

- https://www.forbes.com/advisor/banking/open-banking/#:~:text=Open%20banking%20in%20the%20U.S.,%C2%AE%2C%20use%20open%20banking%20software

- WorldPay Global Payments Report (2022)